- The 99 - a newsletter by GFY

- Posts

- 💛 The last day to claim your free will 🌸 What the spring statement means for you 🏡 A handy stamp duty table

💛 The last day to claim your free will 🌸 What the spring statement means for you 🏡 A handy stamp duty table

The 99 - 10 February 2025

Good morning and welcome back to The 99: the home of financial news and insights made simple. You can count on accessible, trustworthy, and unbiased news insights every Monday.

After a short two-week break we’re back with your usual round-up of must-know financial stories. Thank you for bearing with us.

A reminder that the free will campaign ends TODAY. Last Autumn we worked with the brilliant team at Octopus Legacy to give anyone who wants one, a free will in partnership with charities across the UK - with the GFY community raising £1,298,190 for charity through gifts left in wills 🎉🎉🎉

The campaign is back meaning you can write or update your will for FREE using GFY’s link until midnight tonight.

You can write your will

👩💻 Online

📲 Over the phone

👥 Face-to-face

The cost of the will is covered by whichever charity you choose, saving you up to £150 – many choose to leave a gift to charity as a thank you - but it isn’t required to claim the free will offer.

Struggling to view the whole email? Somewhere above this text you’ll see ‘view on web’.

As always, if you have any feedback, questions or content requests, just reply to this email. We would love to hear from you.

Alice & the GFY team x

.png)

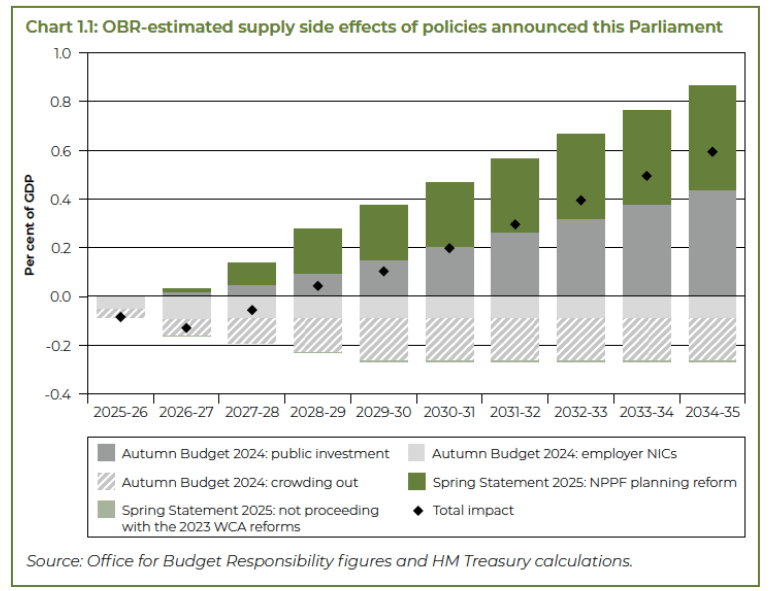

The Spring Statement & What It Means for You?

On Wednesday March 26, the Chancellor of Exchequer, Rachel Reeves delivered the Spring Statement* to Parliament.

The statement addressed budget and public spending reforms, defence, infrastructure, housing and the UK’s economic outlook, with ‘growth’ being the overall priority or central focus of the initiatives.

*Spring Statement - An annual statement delivered by the Chancellor of the Exchequer to the provide an update on the health of the UK economy, based on the latest forecasts from the Office for Budget Responsibility (OBR)

📢Key Announcements 📢

Public Service Transformation 🔄

Reducing administrative budgets by 15% by the end of the decade, with savings on back-office functions of £2.2 billion per year and ensuring that front line services are prioritised.

NHS England will be brought back into the Department of Health and Social Care to reduce bureaucratic inefficiencies and duplications.

Creation of a £3.25 billion Transformation Fund to support the fundamental reform of public services, seize the opportunities of digital technology and Artificial Intelligence (AI), and transform frontline delivery.

Resource Departmental Expenditure Limit (RDEL)* will grow at 1.2% in real terms.

*Resource Departmental Expenditure Limit (RDEL) refers to the spending limit set by the UK government for the day-to-day running costs of its departments.

Welfare & Benefits Reforms 🫂

The Universal Credit health element will be frozen for existing claimants until 2029-30. For new claims, it will be reduced to £50 a week in 2026-27 and then frozen until 2029-30.

Increase in the standard allowance for new and existing claims above inflation from April 2026.

Increased checks on potential Universal Credit claimants by introducing more ways to verify the amount of savings they hold, as well as their earnings and expenses to save.

Recruitment of over 500 additional DWP fraud and error staff who will make better use of government data to correct errors in benefit claims.

Review of the PIP* assessment, and getting more people into better jobs while protecting those who cannot work due to ill health.

PIP - Personal Independence Payment assessment refers to money from the government to help people with long-term physical or mental health conditions or disabilities

Closing the Tax Gap 💰 (i.e., Grow government income from tax debts)

At the end of Dec 2024, taxes owed to the government was over £44bn, over double the amount, five years ago.

She announced different measures to make it easier for people to pay taxes and for the government to recover outstanding tax debts, while keeping Labour’s promise of no tax rises.

Some of these measures include investing in HMRC’s compliance & debt management capacities, making tax digital, increasing late payment penalties, making better use of third party data etc.

These are expected to raise over £1 billion in additional gross tax revenue per year by 2029‑30.

Strengthening Defence 🛡️

The government seeks to strengthen national security, drive growth, and keep the British people safe and secure.

It is providing a £2.2 billion uplift to the Ministry of Defence budget for 2025-26, and has committed to increase spending on defence to 2.5% of GDP from April 2027 which will be funded from international aid (Official Development Assistance budget).

Other initiatives such as investments in advanced technology such as Directed Energy Weapons, UK Defence Innovation, buy‑back the MOD Service Families housing stock and enhance the UK’s programme of joint exercises with NATO allies.

Investing in Growth through Housing, Infrastructure and Skills 🏘️ 🛣️

Increasing capital spending by £13 billion to support growth-enhancing investments including infrastructure, housing, and defence innovation.

Investing £2 billion in social and affordable housing in 2026-27, which will deliver up to 18,000 homes. The OBR expects that this willl raise economic growth by 0.2% and add £6.8 billion to the economy by 2029‑30.

Committing £625 million to address large-scale skills shortages in the construction sector, to deliver the government’s plans to build 1.5 million homes in England and progress vital infrastructure projects.

Other financial commitments to create construction‑focused skills bootcamp places, new construction Foundation Apprenticeships, and new Teacher Industry Exchange Schemes.

Economic & Fiscal Outlook 📈 - Growth, Inflation, Interest Rates

The OBR expects slower growth in 2025, hence, reducing its growth forecast from 2% to 1%, but expects growth to pick up from 2026 over the next four years.

Inflation will peak at 3.8% in July 2025, before falling close to the 2% target from Q2 2026.

Higher standards of living and increases in real wages and real household disposable incomes are also expected over the period (Q3 2024 – Q2 2029).

What does this mean for you?

🔍 Navigating Uncertainty

The Chancellor highlighted global economic uncertainty and changes for which the UK is not immune such as global financial markets volatility, increasing bond yields, volatile oil prices etc.

Within the UK, the impact of these welfare and public sector reforms may be felt through income losses, or redundancies.

Cautious spending and reassessment of financial priorities will help to cushion the impact.

⏫ Maximising Opportunities

Despite the downsides, the statement also highlights higher standards of living in the long run with opportunities and investments in certain sectors like construction, housing, defence and defence tech, innovation, AI, R&D etc.

Focus on maximising these opportunities, either through upskilling, seeking opportunities, jobs or investing in these sectors.

STAMP DUTY DEADLINE TOMORROW: How much will it cost buyers in 2025

If you're buying a home in England or Northern Ireland, tomorrow is the final day to benefit from the current stamp duty reliefs -after that, the charges are going up.

🏠 What’s changing?

From April 2nd, stamp duty will cost buyers more—especially first-time buyers around the £425k–£625k range, who stand to lose thousands if they don't complete by tomorrow.

💸 How Much More You’ll Pay After April 1

Property Price | Current Stamp Duty (Home Mover) | From April 2 (Home Mover) | Increase (Home Mover) | Current Stamp Duty (FTB) | From April 2 (FTB) | Increase (FTB) |

£125,000 | £0 | £0 | £0 | £0 | £0 | £0 |

£250,000 | £0 | £2,500 | £2,500 | £0 | £0 | £0 |

£425,000 | £8,750 | £11,250 | £2,500 | £0 | £6,250 | £6,250 |

£500,000 | £12,500 | £15,000 | £2,500 | £3,750 | £10,000 | £6,250 |

£625,000 | £18,750 | £21,250 | £2,500 | £10,000 | £21,250 | £11,250 |

£750,000 | £25,000 | £27,500 | £2,500 | £25,000 | £27,500 | £2,500 |

£925,000 | £33,750 | £36,250 | £2,500 | £33,750 | £36,250 | £2,500 |

£1million | £41,250 | £43,750 | £2,500 | £41,250 | £43,750 | £2,500 |

💬 What this means for buyers

First-time buyers purchasing a £625,000 home could pay £11,250 more in stamp duty if their deal completes even a day late.

And home movers at the same price? You’ll be facing £21,250 in charges from Tuesday.

Women More Likely to Go Insolvent Than Men – And Have Been Since 2014

Insolvency is when someone can’t afford to pay their debts – and while it’s often associated with bankruptcy, that’s just one type.

Others include Debt Relief Orders (DROs) and Individual Voluntary Arrangements (IVAs).

In 2024, women in England and Wales were more likely than men to become insolvent – marking the 11th year in a row that this has been the case.

According to new figures from the Insolvency Service, the female insolvency rate was 26.5 per 10,000 adults, compared to 22.1 for men. This gender gap didn’t always exist.

Before 2014, men were more likely to go insolvent – but the gap began to narrow in 2009 and then reversed.

One reason is the increased use of DROs and IVAs, which women are more likely to take than men.

Men, on the other hand, are still more likely to go bankrupt.

🤔So what’s behind the difference?

Experts say the trend highlights deeper financial vulnerabilities that disproportionately affect women:

Lower average incomes, but higher average living costs

Childcare and caring responsibilities limiting earning potential

A higher likelihood of managing finances as a single parent

The ongoing gender pay gap

Simon Trevethick from StepChange Debt Charity said nearly two-thirds of their clients are women, with many having higher outgoings and lower earnings than men.

Grace Brownfield from National Debtline echoed the concern, noting that insolvency data “suggests women continue to face greater financial vulnerability in society.”

📍 Where insolvency hits hardest

According to the Insolvency Service, these were the local authorities with the highest and lowest insolvency rates in 2024 (per 10,000 adults):

Highest rates | Lowest rates |

Halton – 64.0 | Kingston upon Thames – 9.5 |

Kingston upon Hull – 53.5 | Wandsworth – 10.4 |

Blackpool – 50.1 | Westminster – 10.5 |

Stoke-on-Trent – 47.1 | Epsom and Ewell – 10.8 |

Nuneaton and Bedworth – 46.7 | Camden – 10.9 |

The North East has had the highest regional rate every year since 2008. London, meanwhile, continues to have the lowest.

💡 If you’re struggling with debt There are free and confidential services that can help. No debt problem is too big to solve.

StepChange: www.stepchange.org

National Debtline: www.nationaldebtline.org

Want to talk it through, ask a question or share your experience? Join the GFY community forum — it's free, supportive with over 1800 of us here to help 💛

Sources/Read More:

The Spring Statement & What It Means for You?

STAMP DUTY DEADLINE: TOMORROW: How much extra could you pay if you miss it?

Women More Likely to Go Insolvent Than Men – And Have Been Since 2014